This summary covers the three keynote presentations delivered at the roundtable: (1) ACE on the regional clean power and PPA policy landscape, (2) BloombergNEF on the economics and demand outlook for clean power in Thailand, and (3) HSBC on corporate PPA structures and bankability requirements. Then, followed by a synthesis of the interactive roundtable discussion and a set of cross-cutting observations. The roundtable was held under the Chatham House Rule.

1. ASEAN Centre for Energy: Clean Power Development and PPA Policies across ASEAN

Presenter: Dr. Ambiyah Abdullah, Senior Economist, Energy Modelling and Policy Planning Department, ACE

1.1 Regional demand and investment context

ASEAN energy demand grew 13.6% between 2019 and 2024, driven by an average 4% GDP growth outlook and a population of 693 million. Fossil fuels still supplied 72% of the region’s electricity in 2024, though the renewables share of generation rose from 18.8% in 2014 to 28% in 2024, with renewables now accounting for 33.7% of installed capacity. The ASEAN Plan of Action for Energy Cooperation targets 45% RE in installed capacity by 2030, with collective regional targets of 40 to 51% of generation by 2035 and 65 to 71% by 2050. Thailand stands at 16,410 MW of renewable capacity, representing 29.4% of its installed base, against a national target of 51% of power generation by 2037.

Estimates of the region’s 2030 energy investment gap range widely, from USD 68 billion (IEA, 2024) to USD 200 billion (ISEAS), with recurring barriers including limited concessional and grant-based finance, persistent regulatory uncertainty, and weak financial ecosystems. ACE’s investment survey ranks PPP, private equity and joint venture structures as the leading instruments for scaling energy investment, with blended finance third and green bonds and loans fourth.

1.2 PPA market structures across the region

| Country | Market structure | Corporate PPA permitted |

| Philippines | Competitive retail | Yes |

| Singapore | Liberalised retail | Yes |

| Indonesia | Single buyer | Limited |

| Malaysia | Single buyer | Limited |

| Thailand | Single buyer | Limited |

| Vietnam | Single buyer | Limited |

| Brunei, Cambodia, Lao PDR, Myanmar, Timor-Leste | Single buyer | No |

Most ASEAN power markets remain single buyer, with only the Philippines and Singapore permitting corporate PPAs without restriction. Three enabling mechanisms can open direct procurement within single-buyer markets: third-party access or wheeling over the state grid for a charge, quota schemes that cap the volume or number of participants, and renewable energy certificates that verify and allow companies to claim renewable use.

1.3 Thailand’s Direct PPA framework in regional context

Thailand announced its Direct PPA framework in October 2025: a 2,000 MW pilot primarily targeting data centre companies, operating through two models — Utility Green Tariff (UGT) and Third-Party Access (TPA). Malaysia’s Corporate Renewable Energy Supply Scheme (CRESS), which provides a pre-allocated quota for commercial and industrial businesses to contract directly with renewable developers and wheel power over the national grid, is the closest regional comparator.

1.4 Regional integration and de-risking

The ASEAN Power Grid extends the PPA model to regional scale. As of 2024, 8 of 18 identified interconnections are operational, with 2.8 GW of grid-to-grid and 7.5 GW of generation-to-grid capacity. A total of 266 GWh has been traded through the Lao PDR-Thailand-Malaysia-Singapore Power Integration Project, with 13.7 GW of interconnection capacity planned by 2040. Given typical PPA tenors of 10 to 20 years, ACE identifies five de-risking approaches to improve bankability: credit guarantees, insurance, power market hedging, multi-buyer models and hybrid PPAs. The forward agenda calls for formalising procurement regulations, standardising PPA templates, establishing REC schemes, and harmonising cross-border PPA and REC rules alongside grid modernisation.

2. BloombergNEF: Enabling Clean Power Access for Thai Corporations

Presenter: Felix Kosasih, Southeast Asia Associate, BloombergNEF

2.1 Cost economics: renewables have won on price

The central message of the BNEF presentation is that the economic case for renewables in Thailand is settled. Firmed solar, modelled as solar paired with a four-hour lithium-ion battery, is already cost-competitive with thermal generation. The 2025 mid-point LCOE for solar-with-storage stands at USD 79 per MWh, in line with combined-cycle gas (USD 82) and below coal (USD 85). Standalone solar is substantially cheaper at USD 47 per MWh. Onshore wind remains comparatively expensive at USD 110 per MWh, reflecting Thailand’s weaker wind resource.

| Technology | 2025 LCOE, mid-point (USD/MWh) | 2050 LCOE, mid-point (USD/MWh) |

| CCGT (gas) | 82 | 80 |

| Coal | 85 | 92 |

| Solar | 47 | 21 |

| Solar with storage | 79 | 38 |

| Onshore wind | 110 | 54 |

| Onshore wind with storage | 140 | 68 |

| 100% hydrogen (CCGT blend) | 302 | 296 |

| 100% ammonia (coal co-firing) | 367 | 259 |

The presentation also addresses the policy debate around clean molecules. Hydrogen blending and ammonia co-firing are not cost-viable decarbonisation pathways for Thailand, either now or through 2050. By 2050, solar-with-storage falls to USD 38 per MWh against USD 259 for full ammonia co-firing. This finding removes the main economic argument for preserving thermal assets as a long-term transition hedge.

2.2 Market structure: corporates are routing around the single-buyer system

Between 2020 and 2024, corporate own-use clean power grew rapidly while utility-scale procurement stagnated. Renewable generation under the Independent Power Supply mechanism grew 129% (3.1 to 7.1 TWh) and SPP Direct grew 127% (0.5 to 1.2 TWh), while utility solar grew only 2% and utility wind 9%. The pattern reflects corporate self-supplying where regulation has not kept pace with demand. The Direct PPA framework can be read as policy catching up with behaviour already well established in the market.

2.3 Data centres as the anchor demand segment

BNEF’s regional scoring places Thailand fifth of six major Southeast Asian markets for data centre attractiveness (score 49.2), with energy availability identified as a key gap. Despite this, the demand outlook is steep: Thailand’s data centre power demand could grow seventeen-fold from 2025 to roughly 31 TWh by 2050 (New Energy Outlook 2026). Most major data centre developers active in Thailand carry firm clean power targets — AWS, Google, DayOne, NTT GDC and Etix Everywhere all target 100% by 2030, ST Telemedia 85% by 2028, and Bridge Data Centers 100% by 2040. There is a deep, creditworthy and target-driven offtaker base waiting for a procurement route.

2.4 Procurement access gaps

Thailand currently offers onsite PPAs, international RECs, and a green tariff (UGT, launched 2025), but only net billing rather than net metering, with exports credited well below the retail rate and not permitted at all for commercial and industrial users. Offsite PPAs remain under discussion, and there is no domestic REC scheme or retail choice. In regional comparison, the Philippines and Singapore offer the fullest procurement menus, while Indonesia is the most restricted. Thailand sits mid-table, with the Direct PPA framework as the key pending unlock.

3. HSBC: Direct Corporate PPAs in Thailand — Why Bankability Matters

Presenter: Benjamin Treves, Senior Manager, Sustainable Finance and Transition, HSBC

3.1 Procurement options for commercial and industrial customers

HSBC maps four routes for C&I customers to decarbonise electricity supply: a standard supply contract, a green tariff contract, renewable asset ownership, and a renewable PPA. The PPA route requires no capital expenditure, carries no operational or delivery risk, and can achieve competitive pricing. Its drawbacks are long-term lock-in and a structural bias toward scale: a company’s size and credit standing determine its ability to negotiate and sign, and smaller companies may struggle to access the market at all.

3.2 PPA structures and market evidence

Four contract structures are defined: onsite or private wire PPA (third-party-owned generation at source), physical PPA (offtaker takes ownership of power generated offsite), sleeved PPA (adds a back-to-back contract with a utility to enable the trade), and virtual PPA (no physical delivery; acts as a financial hedge between offtaker and developer). US market data shows virtual PPAs dominating where regulation permits (24.6 GW of 28.3 GW signed in 2024). In Asia Pacific, 2024 was a record year at over 10 GW, with RE100 adoption growing faster in APAC than any other region since 2019.

HSBC’s recommended corporate approach combines three layers: build out onsite generation and storage, procure green PPAs for residual demand, and optimise demand use and profile. Grouped PPAs, aggregating demand across multiple buyers, were flagged as an emerging route for smaller, lower-rated clients to access the market.

3.3 The bankability argument

The core argument is a causal chain: a bankable contract attracts cheaper capital, cheaper capital lowers the LCOE, and a lower LCOE drives wider adoption. Energy security is framed as a function of how quickly capital can be deployed, which depends on how financeable the underlying contracts are.

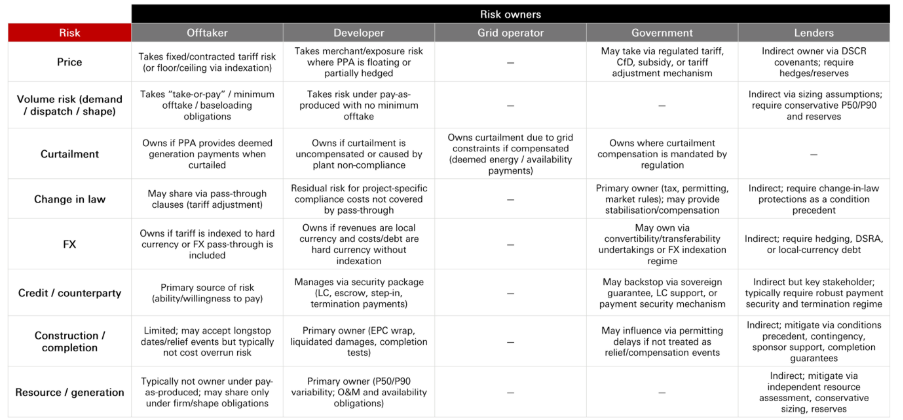

Lenders assess eight factors: regulatory and policy consistency, offtaker credit quality (ideally investment grade, or buyer consortia that spread credit risk), PPA structure and tenor (15 to 25 years preferred), financing availability and cost, grid and curtailment risk, land and development risk, supply chain exposure, and risk allocation. Clear allocation of price, volume, curtailment, change-in-law, FX, credit, construction and resource risks across offtaker, developer, grid operator, government and lenders accelerates credit approval. The path to execution runs through six stages: load and site assessment, structure selection, term sheet, credit package, grid and metering, and financial close.

3.4 Case study: Malaysia’s Corporate Green Power Programme

HSBC’s inaugural CGPP financing (signed May 2025) provides the closest regional precedent for what Thailand is attempting. Approximately MYR 214.6 million (USD 49 million) of senior secured green project finance was arranged for two 29.99 MWac ground-mounted solar projects in Perak and Kedah. The structure comprised a 15-year Islamic project financing, fully amortising, with non-recourse bank guarantees of up to 24 years, structured as a Green Loan. Offtake was via long-term fixed-price corporate green power agreements with majority investment-grade buyers including Texas Instruments and Micron. Long-dated interest rate hedging was cited as critical to achieving financial close.

For peer’s status, Malaysia retains a single-buyer market, yet a clear programme framework with pre-allocated quota and third-party access proved sufficient for international bank-led, 15-year non-recourse project finance backed by corporate offtake. Thailand’s pilot will be judged against whether its detailed rules can produce an equivalent outcome.

4. Roundtable Discussion: Summary of Key Points Raised

The interactive roundtable was moderated by Justin Wu, Head of Sustainability and Climate Change, Asia and Middle East, HSBC. The following paragraphs reflect the substantive points raised across participants, presented without attribution in accordance with the Chatham House Rule.

4.1 Buyer perspective

Corporate demand for decarbonisation remains firm despite the prevailing global uncertainty, driven particularly among export-oriented industries by the EU’s Carbon Border Adjustment Mechanism and by supply-chain requirements imposed by multinational customers.

However, many Thai companies, especially in domestic industries, emain hesitant to commit to targets such as RE100, not from a lack of willingness but from uncertainty over what such commitments entail and how to act on them practically. Physical constraints on grid access compound the difficulty of securing resilient clean power supply, and it was noted that the DPPA framework is precisely the kind of instrument designed to address this gap. As a policy tool, both the UGT and DPPA models should be designed to accommodate the varied needs of corporate buyers across locations and load profiles. A key outstanding concern raised by multiple participants is that the total all-in cost of accessing power through the framework remains unknown. This includes wheeling charges and other pass-through costs, and the uncertainty constrains corporate planning.

Participants from energy-intensive industrial sectors noted that data centres are not the only constituency for direct procurement. Industrial estates and large manufacturing sites have comparable or larger energy needs, and the framework’s design should account for this broader demand base. One participant noted that the Eastern Economic Corridor alone has 17 confirmed data centre projects with a further 47 submitted, representing a combined declared power demand of the order of 17,000 MW though the credibility of a portion of this declared pipeline was questioned.

Several participants emphasised that onsite renewable generation (e.g. rooftop and ground-mounted solar) has in many cases already been exhausted or constrained by site and connection limits. For large industrial conglomerates committed to net-zero targets, direct procurement through the DPPA framework is therefore not an alternative to onsite generation but the logical next step once onsite potential is depleted.

4.2 Developer perspective

Developers expressed strong readiness to supply green power and confirmed they can move faster if the commercial and regulatory environment is workable. The central concern raised was the level and transparency of wheeling charges, which multiple participants described as currently too high relative to the tariff levels at which renewables can be competitively sold. One participant noted that recent tenders for solar and wind came in at approximately THB 2 and THB 3 per unit respectively, while the UGT tariff sits at around THB 4 per unit — a spread that, after wheeling and other charges are factored in, may leave direct procurement economically unattractive relative to the grid. The view was expressed that wheeling charges for UGT and DPPA should be closer to THB 1 or below, based on analysis by the Energy Research Institute, and that EGAT, PEA and MEA should undertake a fresh calculation reflecting the evolving generation mix.

A further structural issue identified is the challenge of balancing renewable supply against corporate demand at the sub-meter level. Intermittency and demand-shape mismatches are manageable through portfolio diversification across technologies and locations, but the framework needs to define imbalance rules and settlement mechanics clearly enough for developers to price and for lenders to model. One participant noted that UGT, as currently structured, risks being seen as a barrier to rather than an enabler of broader renewable energy adoption, since it embeds the legacy single-buyer cost structure rather than creating a genuinely competitive route to market.

4.3 Financier perspective

From the financing side, the emphasis was on risk allocation as the precondition for underwriting. Where risks are clearly assigned among the offtaker, developer, grid operator and government, lenders can price and structure around them; where they are undefined or sit ambiguously with multiple parties, transactions stall. Blended finance structures were identified as tools to improve bankability for early pilot transactions, particularly where offtaker credit or regulatory frameworks do not yet meet conventional underwriting requirements. ADB’s existing facilities, such as the one for Monsoon Wind, are one example. The point was made that the policy gap, rather than the financing gap per se, is the binding constraint in Thailand: instruments exist, but the regulatory clarity to deploy them at scale does not.

5. Cross-Cutting Takeaways

- Economics is no longer the constraint; market access is. Firmed solar is already at parity with gas, yet utility-scale procurement has stagnated while corporate own-use supply grew by more than 125% in four years. The binding constraint on clean power deployment is regulatory architecture, not cost. This reframes the Direct PPA debate: the question is whether the rules will allow capital to reach projects that already make economic sense.

- Wheeling charges are the make-or-break variable. The roundtable discussion converged on this more sharply than any other issue. At current indicative levels, the all-in cost of power through the UGT and TPA routes may not be commercially attractive to a wide range of buyers. A transparent, independently verified wheeling charge methodology is therefore the single most important regulatory output of the pilot, and its absence is the principal planning obstacle for buyers, developers, and lenders alike.

- Bankability is the bridge from policy to projects. HSBC and ACE converge on the same conclusion: the pilot’s success depends on whether wheeling charges, curtailment rules, change-in-law provisions, and credit structures are defined clearly enough for lenders to underwrite 15-year-plus financing. The Malaysian CGPP transaction demonstrates that a single-buyer market with a clear programme framework can support non-recourse corporate PPA project finance. Thailand’s framework will be assessed against that precedent.

- The demand base is broader than data centres. The pilot is framed around data centre offtakers, but industrial conglomerates facing net-zero supply-chain requirements, and whose onsite generation potential is already exhausted, represent an equally significant and arguably more politically durable constituency. Framework design and quota allocation should reflect this.

- Access equity remains an open design question. The bankability logic privileges large, investment-grade offtakers. Aggregated or grouped PPAs, credit enhancement structures, and simplified standard contracts are the mechanisms through which smaller Thai companies can eventually participate. These deserve a place in framework design rather than being deferred to a later phase.

- Thailand’s regional competitiveness is at stake. Thailand ranks fifth of six in Southeast Asia for data centre attractiveness, partly on energy availability. A credible, bankable DPPA framework is as much an investment-attraction instrument as a decarbonisation tool, and the cost of delay is measured in capacity and capital flowing to Malaysia and Indonesia instead.