On April 28, the Climate Finance Network Thailand (CFNT), together with the Institute for Energy Economics and Financial Analysis (IEEFA), hosted a webinar titled “Thailand’s Gas Dilemma: From Underutilized to Energy Insecurity.”

The session featured Christopher Doleman, a researcher at IEEFA and co-author of the report “Thailand’s Gas Conundrum: Overbuilt, Underutilized, and Increasingly Expensive.”

Christopher explained the structural risks that excessive gas dependence brings to Thailand’s energy system, while also highlighting more promising opportunities for transitioning toward renewable energy in the future.

Thailand’s Growing Dependence on LNG

Thailand developed its gas resources as a means of diversifying away from oil following the twin oil crises of the 1970s. Over the following decades, gas has gradually become embedded in the country’s economy.

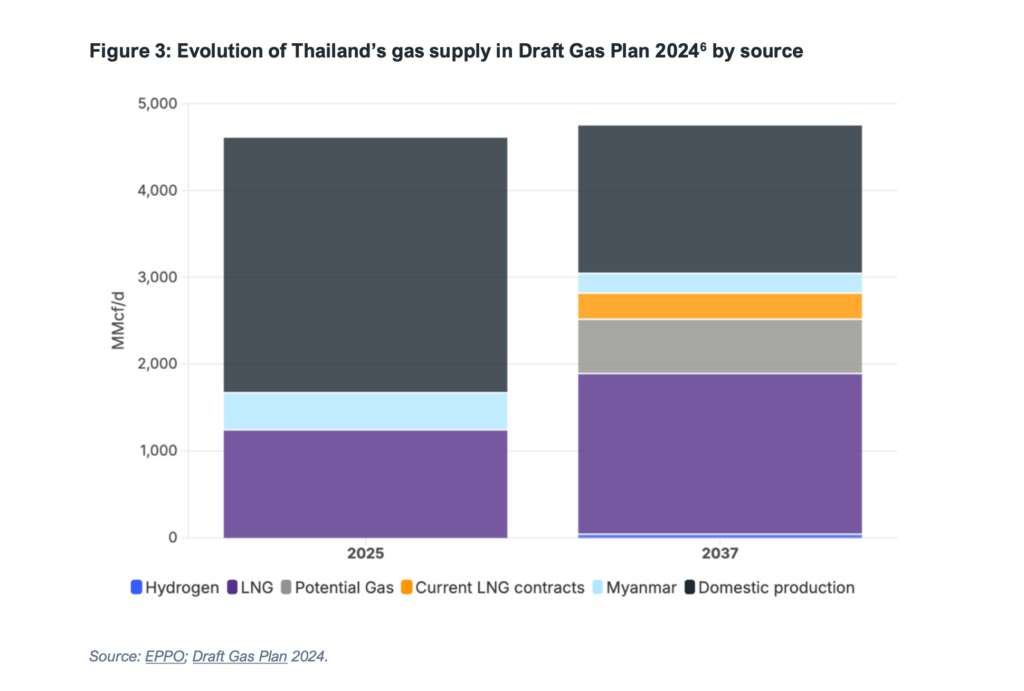

Over the last decade, Thailand’s gas resources have entered structural decline, leaving LNG imports to fill the void. In the 2020s, the share of gas supply met by LNG imports has almost doubled to 27%.

With LNG’s sourcing costs double that of domestic production, Thailand’s gas supply is structurally getting more expensive. The government frequently restructures gas pricing in an attempt to balance the rising cost across stakeholders. However, with economic fortunes suppressed by a shaky pandemic recovery, consumers and businesses have little ability to absorb the burden of higher costs.

Despite this worsening affordability challenge, Thailand has continued to plan for a future where gas remains embedded in the economy. The last Draft Power Development Plan (Draft PDP 2024) released–but not enacted– in 2024 called for 6.3GW of new gas-fired facilities. This would increase the share of LNG imports from 27% today to between 39 and 46% by 2037, depending on the success of offshore exploration in the Gulf of Thailand and off the coast of neighboring Myanmar.

However, the government’s suspension of 4GW of gas-fired capacity and delayed commissioning of the Burapa power plant in October 2025 due overcapacity suggests that the existing fleet is underutilized and that further gas expansion may not be required.

Drivers Thailand’s electrical overcapacity

Christopher highlighted several drivers of Thailand’s electrical overcapacity:

- A sluggish pandemic recovery and verly optimistic GDP projections

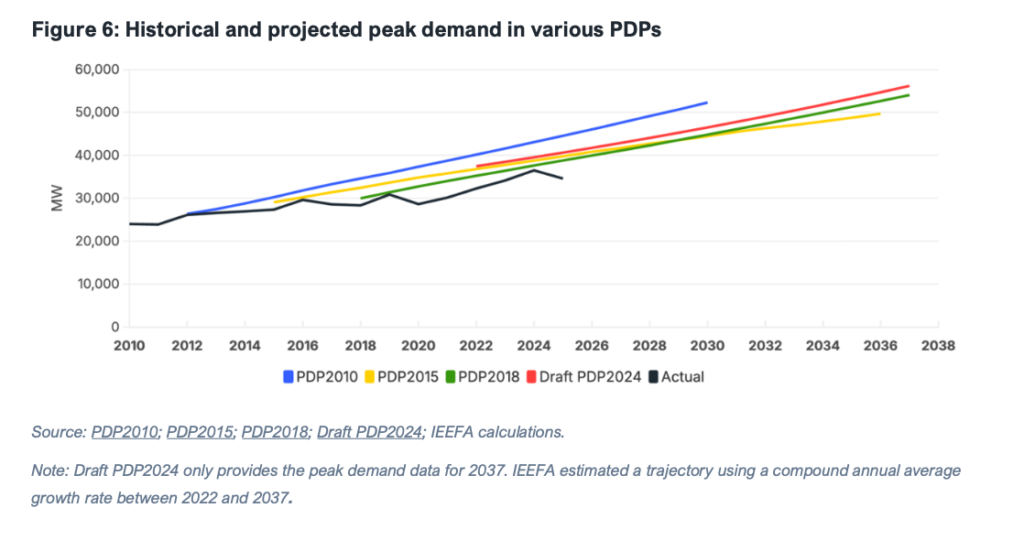

The Thai economy was expected to grow more in line with the global average but ended up lagging advanced economies, growing around 2.2% per year since 2020.

Since the government is modelling electricity demand peaks and capacity expansions to meet what turned out to be an overly optimistic GDP projection. Without that economic growth, the demand has not materialized.

- Focus on maintaining an excessive reserve margin

Historically, the expansion plans in Thailand’s PDPs were bound by a reliability criteria that restricts the reserve margin from falling below 15%. Typically, a healthy reserve margin for a country’s electricity system is around 10–15%.

Moreover, media reports suggest that the government approaches its reserve margin calculation more conservatively by derating the capacity for availability and omitting uncontracted capacity.

As a result, Thailand’s reserve margin reached past 70% in 2020, before falling back to about as high as 55% in 2025, and previously peaked at 70% in 2020. The cost of maintaining this excess capacity is ultimately borne by households, further weakening an already fragile economy.

- Surge in renewables

Utility-scale solar capacity doubled to reach 7.1GW in 2025, and estimates by Transition Zero suggest that rooftop capacity has doubled to reach between 3 and 4.2GW. As a result, generation from solar also almost doubled to reduce the call on gas-fired power.

- Weather

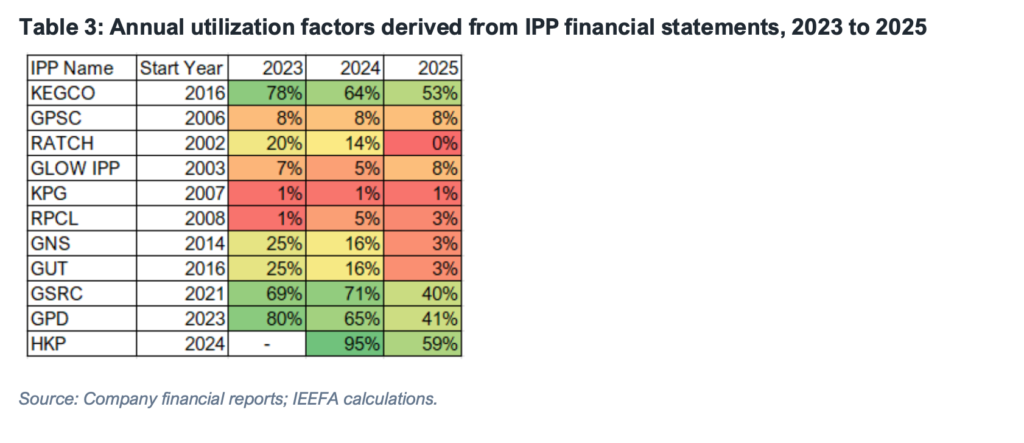

Mild weather played a part. However, an investigation into the utilization of Thailand’s fleet of gas Independent Power Producers (IPPs) suggests that this is a trend and not a 2025 weather-driven anomaly.

Underutilized Gas Power Plants

In 2025, seven of eleven large private gas power plants totalling 11GW in capacity operated at only 10% of their total capacity. More importantly, this problem did not begin last year. Since 2023, this 11GW collective of private gas-fired power plants have operated at under30% of their total generating capacity.

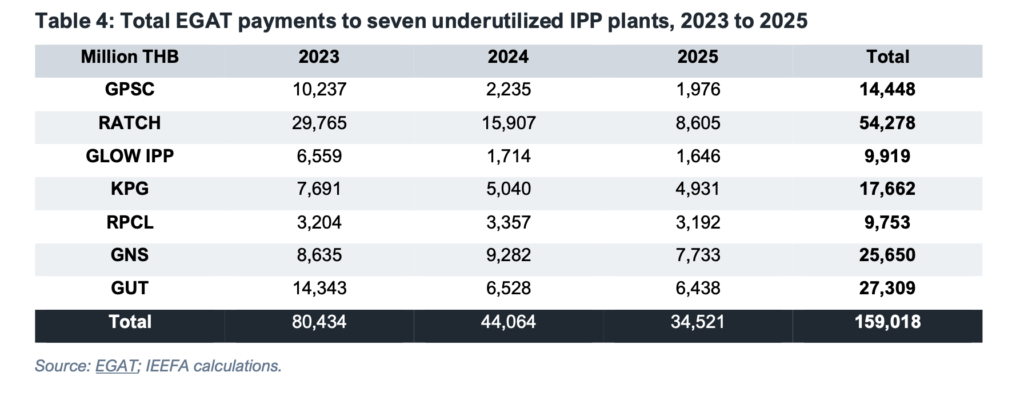

Despite not operating at full capacity, the Electricity Generating Authority of Thailand (EGAT) is still required to pay these plants. IEEFA estimates that since 2023, EGAT has paid a total of 159 billion baht to the seven major private power producers, including 61 billion baht in Availability Payments (AP) to sit idle and . These payments are passed onto consumers.

Thailand’s existing project pipeline faces delays, in part due to rising costs of gas power plants

Previously, EGAT had planned to develop at least five additional power plant projects by 2029 to replace facilities scheduled for retirement. However, these projects have been postponed indefinitely without a clear explanation.

IEEFA’s analysis suggests that rising costs across the gas power plant supply chain could be the primary culprit.

Looking at the terms of the North Bangkok tender, IEEFA estimates that EGAT was expecting the project to cost around USD900 per kW. While this cost would have worked a few years ago, shortages in gas turbines have since caused the capital cost of large-scale gas projects to triple to USD2400 per KW.

This suggests that rapid cost escalation is causing EGAT to cancel or delay project tenders. If so, the turbine shortage could continue to delay and challenge Thailand’s expansionary gas plans.

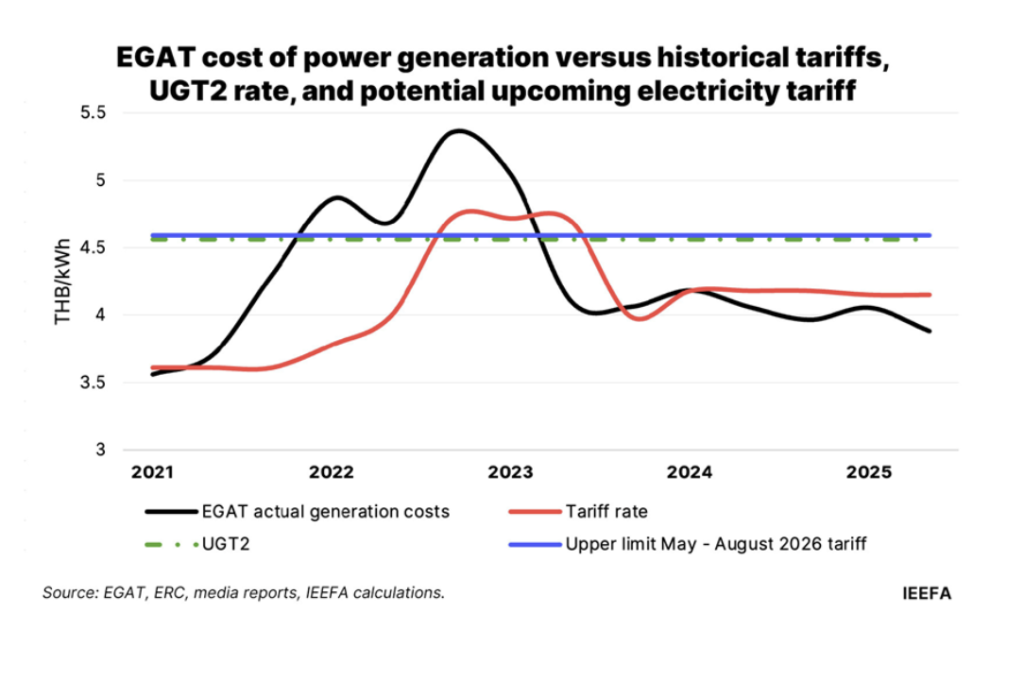

However, if plants are built, there could be inflationary implications for Thai consumers due to their impact on availability payments, the purpose of which are to recoup the capital cost of power plant expansion. In early 2026, availability payments made up 17% of electricity tariffs. A tripling of capital costs will put upward pressure on availability payments, and in turn, consumer tariffs, to the degree that gas expansion occurs under this new cost regime.

EGAT’s Debt Burden could limit future subsidization of electricity rates

During the energy crisis triggered by the Russia–Ukraine war, EGAT acted as a buffer between rising energy prices and consumers. As a result, in 2022 EGAT accumulated debt totaling 150 billion baht. EGAT expected to fully repay this debt by 2028 prior to the West Asia conflict.

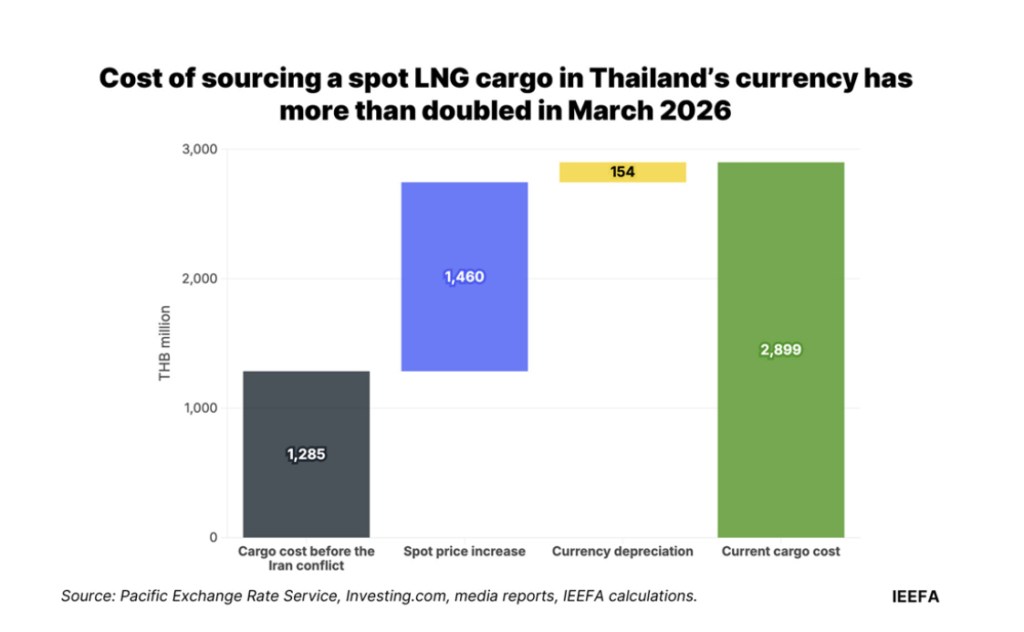

Iran conflict is laying bare the unaffordability of LNG

However, recent tensions involving Iran — including the closure of the Strait of Hormuz and damage to Qatar’s gas production infrastructure — have continued to push global LNG prices upward. Qatar is one of the world’s key LNG producers, accounting for around 3% of the global LNG supply chain. As a result, LNG prices are expected to remain elevated for several years, challenging EGAT’s ability to repay its debt.

Thailand already experienced the impact of such volatility. In March this year, the country purchased an LNG shipment at a price of US$23.5 per million BTU. Account for the depreciation in the baht, this is 225% higher in domestic currency than the price paid in February. Although prices have since eased somewhat, they still remain at least 50% higher than they were before the start of the conflict.

Alternative approaches: Lessons from Pakistan for Thailand

One key question is whether Thailand can realistically transition away from its dependence on LNG. Christopher explored this question by comparing Thailand’s situation with that of Pakistan.

Back in 2022, Pakistan faced a major energy crisis following the Russia–Ukraine war. The Pakistani government struggled to secure LNG supplies, causing electricity prices to surge and widespread blackouts across the country. In response to the crisis, many citizens began installing rooftop solar panels to generate electricity themselves rather than relying on the state electricity system. As a result, Pakistan’s solar sector has expanded more than fourfold over the past three years.

Consumer defection caused grid demand to fall, and Pakistan was looking into ways to defer, divert and resell its surplus LNG cargoes last year. Moreover, the panels did help improve the resilience of the country’s electricity system during the onset of the Iran conflict.

The question, then, is whether a similar phenomenon could occur in Thailand. Christopher pointed to several interesting signals emerging from both the public and private sectors.

First, solar costs continue to decline. Compared with 2022, the cost of importing solar panels from China has fallen by around two-thirds, and is now roughly half the level seen in 2023.

Second, government policy has become more supportive. In recent years, the Thai government has eased several regulations that make solar energy more accessible. For example, installing solar panels is no longer classified as an industrial activity, meaning households and businesses no longer need factory operation permits for installation.

Third, financial incentives are increasing. In March, the government introduced incentives such as a 200,000-baht tax deduction for solar installations. In addition, the upcoming three-tier electricity pricing policy is expected to provide strong incentives for high-consuming households to install rooftop solar systems. Other measures are also being developed to encourage adoption within the business sector.

IEEFA estimates that compared with LNG-fired electricity generation, renewable energy generation is now approximately three times cheaper. Meanwhile, solar-plus-battery systems are estimated to be around twice as cheap as LNG generation.

IEEFA also estimates that electricity generated from its current solar capacity of 7.1 GW could offset 1.3 LNG cargoes a month, forgoing US$900 million in fuel import expenses per year. These savings could help reduce EGAT’s debt burden and support other policies aimed at lowering the cost of living for the public during this multi-commodity crisis.

A New Path Forward for Thailand

Christopher concluded by arguing that the current global and domestic context presents Thailand with a valuable opportunity to reconsider its energy future.

First, several current realities — including the underutilization of gas infrastructure, rising LNG prices, and increasing costs throughout the gas power plant supply chain — are beginning to challenge Thailand’s plans to expand gas-fired power generation.

Second, the crisis involving Iran has worsened the situation further, placing additional strain on Thailand’s already fragile economic structure through rising LNG import costs.

Third, however, this moment also presents an opportunity for Thailand to construct subsequent PDPs in line with these changing realities by prioritizing renewable energy growth over gas expansion. Doing so could help build a more resilient and secure energy system for the future.