The ongoing war in the Middle East is exposing a critical vulnerability in Thailand’s energy system — its heavy dependence on imported liquefied natural gas (LNG).

The US-Israeli joint attack on Iran has triggered a conflict across several parts of the Middle East, including Qatar — the world’s largest LNG exporter and one of the key sources from which Thailand imports LNG.

The conflict is once again challenging the global economy.

For Thailand, however, it exposes something deeper — an energy system that remains heavily dependent on imported LNG.

Middle East war and LNG crisis

Data from JustPow, a coalition of organisations working in the fields of energy and the environment in Thailand, shows that natural gas remains the country’s main source of electricity generation.

Indeed, 58.19% of Thailand’s power production in 2024 used LNG fuel. More than half of this supply comes from domestic gas fields in the Gulf of Thailand, while 35.5% is imported LNG, and the remainder comes from pipeline gas from Myanmar.

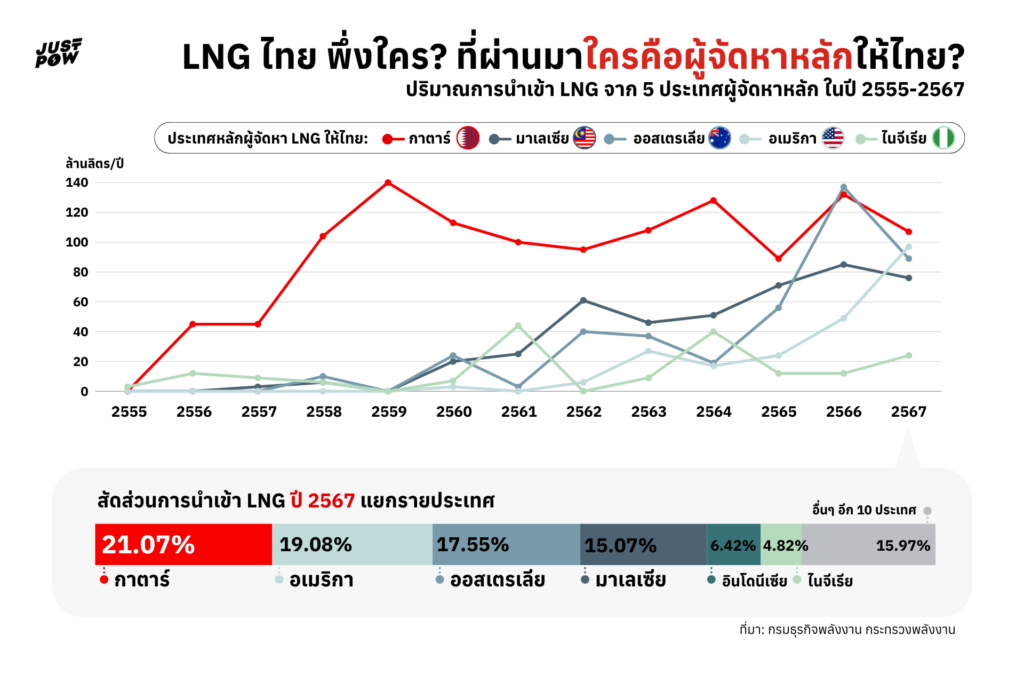

Qatar is the largest LNG exporter to Thailand. Between 2011 and 2024, Thailand imported 1,129.69 million litres from Qatar, far ahead of other suppliers such as Malaysia and Australia.

The Thai government and the Electricity Generating Authority of Thailand (EGAT) have attempted to reassure the public, saying they could diversify LNG imports from other regions and increase production from the Mae Moh coal-fired power plant in Lampang to stabilise electricity prices.

However, energy experts remain concerned about the long-term implications.

Thailand has faced similar problems before. During the height of the Russia–Ukraine war in 2022, global LNG prices surged, forcing Thailand to spend significantly more on LNG imports to produce electricity. The government accumulated debt to EGAT of around US$4.7 billion (155 billion baht) for subsidising electricity prices.

Thai households felt the impact directly. Electricity tariffs exceeded 4 baht per unit for the first time in 14 years, peaking at 4.72 baht per unit in September 2022.

The lesson is clear: when global LNG prices surge, Thai consumers inevitably bear the cost.

Yet the deeper concern lies not only in electricity prices, but in the structure of Thailand’s energy system itself, which remains heavily dependent on fossil fuels.

Stranded fossil fuels

A report by Climate Finance Network Thailand (CFNT), titled “Thailand’s Fossil Lock-In: Stranded Risk of Midstream Oil and Gas Infrastructure”, warns that Thailand is investing heavily in fossil fuel infrastructure that could become stranded assets in the future.

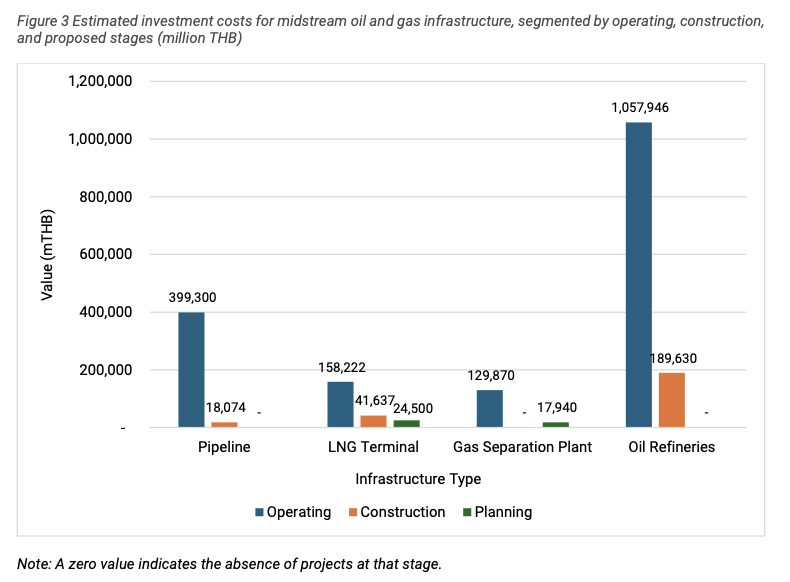

These include more than 84 billion baht in LNG infrastructure, consisting of receiving terminals worth 66 billion baht and gas separation plants worth around 18 billion baht.

In addition, petroleum refinery investments amount to approximately 189 billion baht.

One recent development came when the cabinet, in October 2018, approved the Map Ta Phut port Phase 3 project, allowing Gulf MTP LNG Terminal Company Limited — a joint venture between GULF and PTT Tank — to construct a third LNG terminal.

The decision was made despite ongoing questions about the economic viability of the first and second terminals, which have not yet been fully utilised.

Such projects do more than lock Thailand’s energy future into fossil fuels. Critics warn they risk becoming stranded assets as the world shifts towards renewable energy.

The continued expansion of fossil fuel infrastructure in Thailand raises a critical question: How serious is Thailand about achieving its net-zero target by 2050 under its updated Nationally Determined Contribution (NDC 3.0)?

The risk of false solutions

Under Thailand’s NDC 3.0, submitted last November, the country has set a net-zero target of 2050 and aims to reduce greenhouse gas emissions by 47% by 2035.

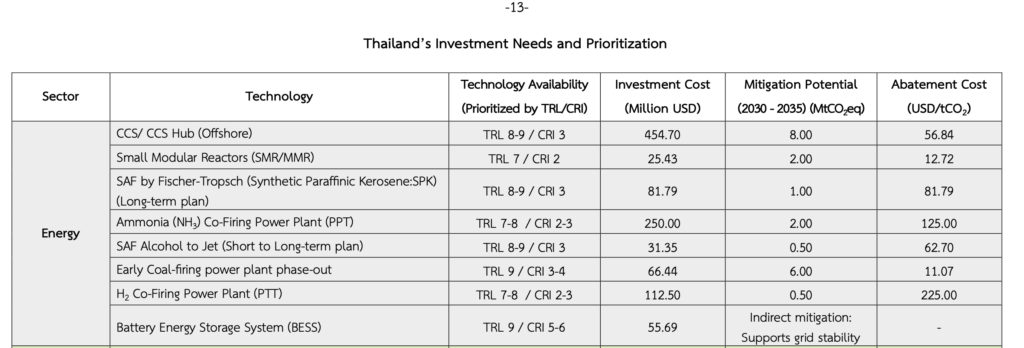

However, rather than pursuing the most effective approach — phasing out fossil fuels — Thailand appears to be exploring ways to make existing fossil infrastructure “cleaner” through major investments in technologies such as hydrogen co-firing and carbon capture and storage (CCS).

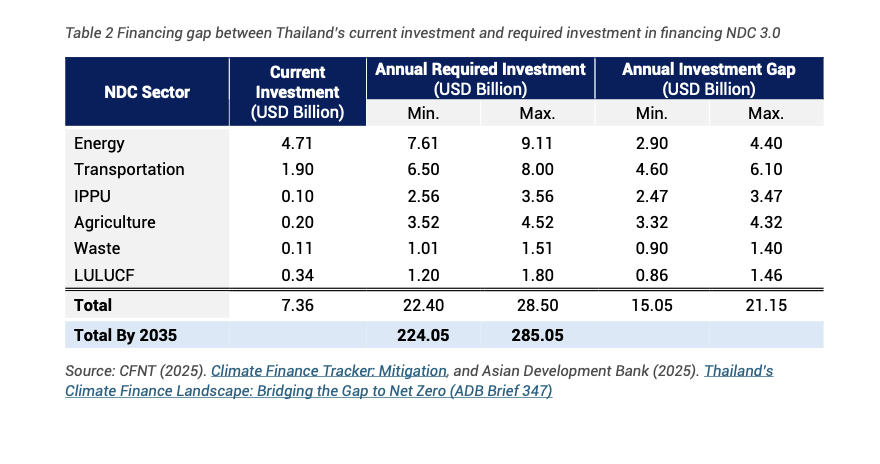

A CFNT report, Financing NDC 3.0: Challenges and Opportunities toward Net Zero 2050, finds that Thailand faces a financial gap of at least $2.9 billion in the energy sector.

At the same time, pursuing “cleaner” fossil pathways could expose the country to substantial financial risks — US$455 billion for CCS and copy13 billion for hydrogen co-firing — while remaining highly uncertain in terms of effectiveness.

By contrast, the report identifies early coal phase-out as the most cost-effective mitigation option — six times cheaper than offshore CCS and 20 times cheaper than hydrogen co-firing.

The primary barrier lies in the power purchase agreements (PPAs) that EGAT has signed with commercial power producers.

However, such contracts are not rigid. In several countries, including Spain, similar agreements have been renegotiated for the public good to facilitate energy transitions.

In other words, the barrier is not technical or legal — it is political. The real question is whether policymakers have the will to act.

Towards a stronger future

If Thailand is serious about achieving its climate goals while safeguarding its energy security, the economic case for renewable energy is already well established.

BloombergNEF’s Thailand: Turning Point for a Net-Zero Power Sector finds that expanding renewable energy is the most cost-effective pathway for the country to achieve its climate targets.

The cost of electricity from solar power combined with battery storage is already lower than that of new gas- or coal-fired power plants and is expected to continue declining.

At this point, the economic case for renewable energy is clear, just as the risks of continued dependence on fossil fuels are increasingly evident.

What remains is not a lack of solutions, but a lack of political will. The direction forward should now be clear: expanding renewable energy while building a more democratic and resilient energy system for Thai society.